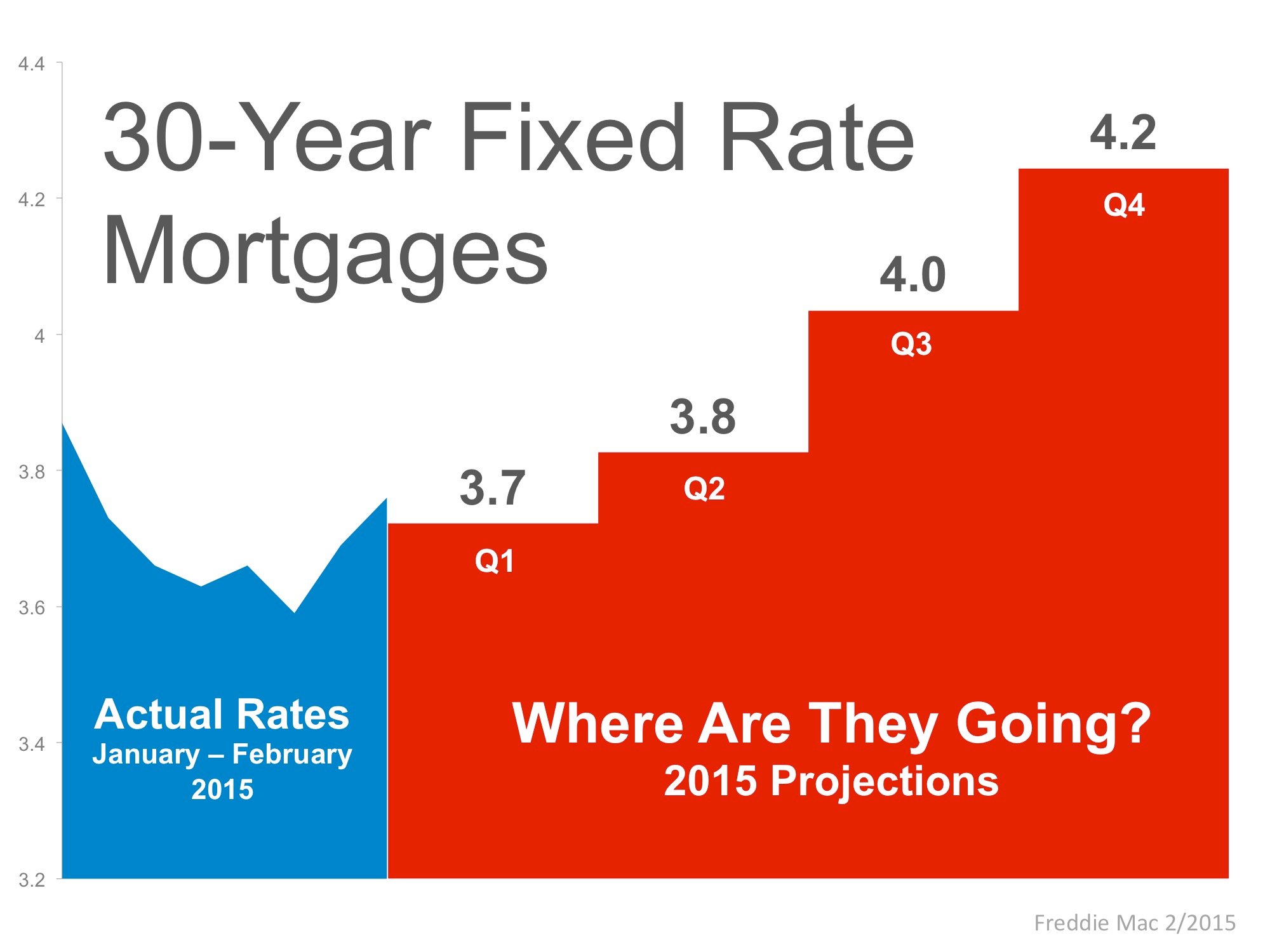

Where Are Mortgage Rates Headed?

The interest rate you pay on your home mortgage has a direct impact on your monthly payment. The higher the rate the greater the payment will be. That is why it is important to look at where rates are headed when deciding to buy now or wait until next year.

Below is a chart created using Freddie Mac’s February 2015 U.S. Economic & Housing Marketing Outlook. As you can see interest rates are projected to increase steadily over the course of 2015.

How Will This Impact Your Mortgage Payment?

Depending on the amount of the loan that you secure, a half of a percent (.5%) increase in interest rate can increase your monthly mortgage payment significantly.

Research released by Zillow touched on this point:

“As rates rise, new home buyers will confront higher financing costs and monthly mortgage payments. For many, this will mean tightening their budgets and sacrificing some luxuries they may take for granted today.”

The experts predict that home prices will appreciate by 4.4% over the course of 2015. If both predictions become reality, families would wind up paying considerably more for their home.

Bottom Line

Even a small increase in interest rate can impact your family’s wealth. To gain a better perspective let’s schedule a meeting to evaluate your ability to purchase your dream home.

Are House Prices Beginning to Accelerate Again?

In a recent post, we explained that the supply of homes for sale in December was at its lowest level in over a year. The January National Housing Trend Report from realtor.com now reveals that inventory in January has decreased another 6.7% month over month and 8.7% year over year. This is occurring at the same time that buyer activity (demand) remains strong.

This prompted realtor.com’s Chief Economist Jonathan Smoke to report:

“January’s inventory data suggest a continuation of the tightening trend we identified last month in the December data, and with a shortage of inventory typically comes increased home prices. Half of the 200 markets realtor.com tracks experienced year-over-year price increases of at least 6% in January.”

This after the National Association of Realtors (NAR) had already reported in their latest quarterly report:

“The majority of metropolitan areas experienced steady but slightly stronger price growth in the fourth quarter of 2014, behind a decline in housing supply and an uptick in demand fueled by lower interest rates and a stronger job market.”

Bottom Line

Whether you are a first time buyer or a move-up buyer, now may be time to purchase a home – before prices increase any further.

Thinking of Buying on the Eastside? What are you waiting for?

If you are planning on becoming a homeowner, or moving up to the home of your dreams in 2015, here are four great reasons to consider buying a home now, instead of waiting until spring.

1. Prices Will Continue to Rise

The Home Price Expectation Survey polls a distinguished panel of over 100 economists, investment strategists, and housing market analysts. Their most recent report projects appreciation in home values over the next five years to be between 11.7% (most pessimistic) and 27.5% (most optimistic).

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

2. Mortgage Interest Rates Are Projected to Increase

Although Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have softened recently, most experts predict that they will begin to rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac & the National Association of Realtors are in unison projecting that rates will be up almost a full percentage point by the end of 2015.

An increase in rates will impact YOUR monthly mortgage payment. Your housing expense will be more a year from now if a mortgage is necessary to purchase your next home.

3. Either Way You are Paying a Mortgage

As a paper from the Joint Center for Housing Studies at Harvard University explains:

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return. That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

4. It’s Time to Move On with Your Life

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise.

But, what if they weren’t? Would you wait?

Look at the actual reason you are buying and decide whether it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer or you just want to have control over renovations, maybe it is time to buy.

If the right thing for you and your family is to purchase a home this year, buying sooner rather than later could lead to substantial savings.

Two Graphs that Scream – List Your Home Today!

We all learned in school that when selling anything, you will get the most money if the demand for that item is high and the inventory of that item is low. It is the well-known Theory of Supply & Demand.

If you are thinking of selling your home, here are two graphs that strongly suggest that the time is now. Here is why…

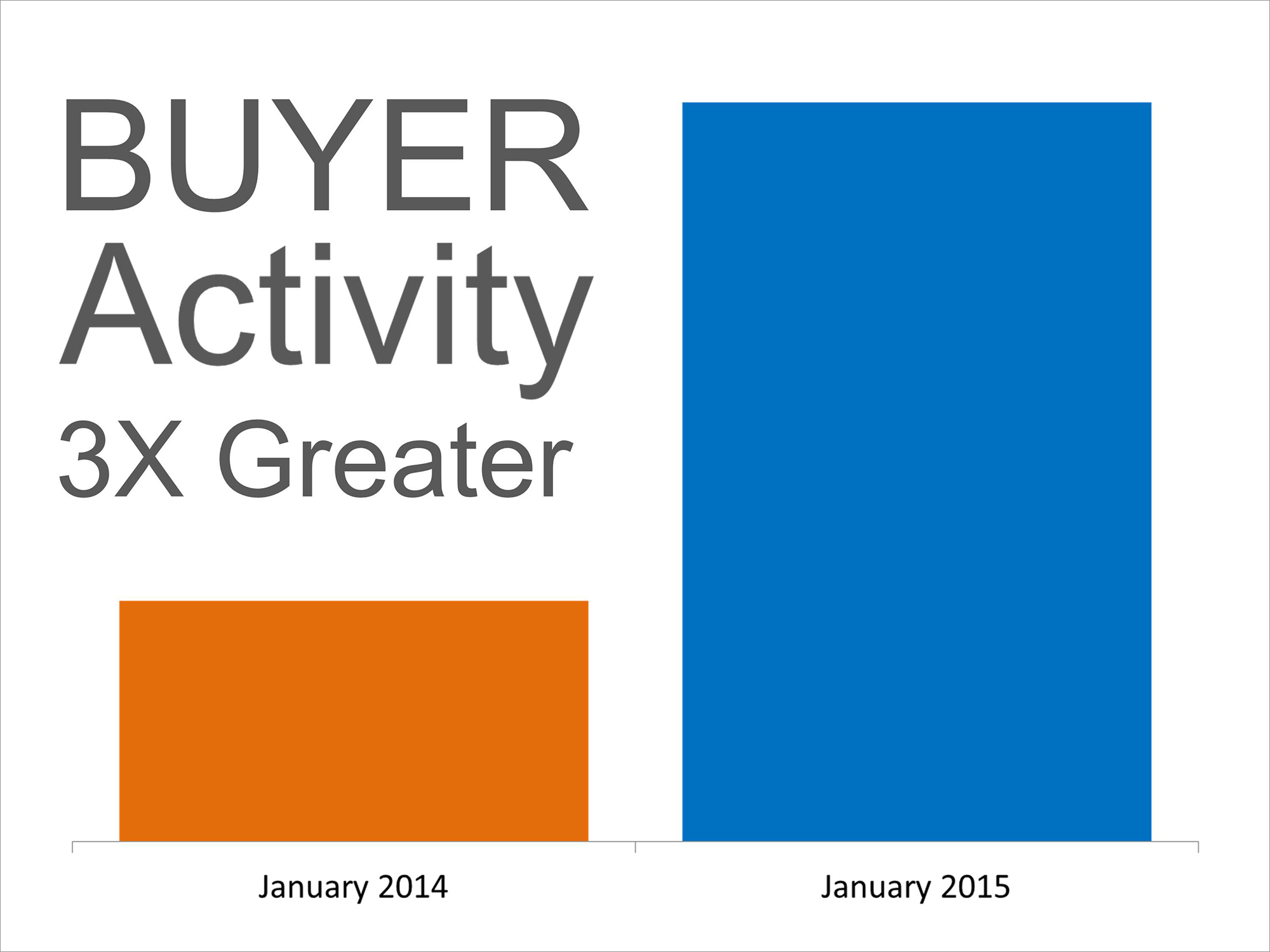

DEMAND

According to research at the National Association of Realtors (NAR), buyer activity last month (January) was three times greater than it was last January. Purchasers who are ready, willing and able to buy are in the market at great numbers.

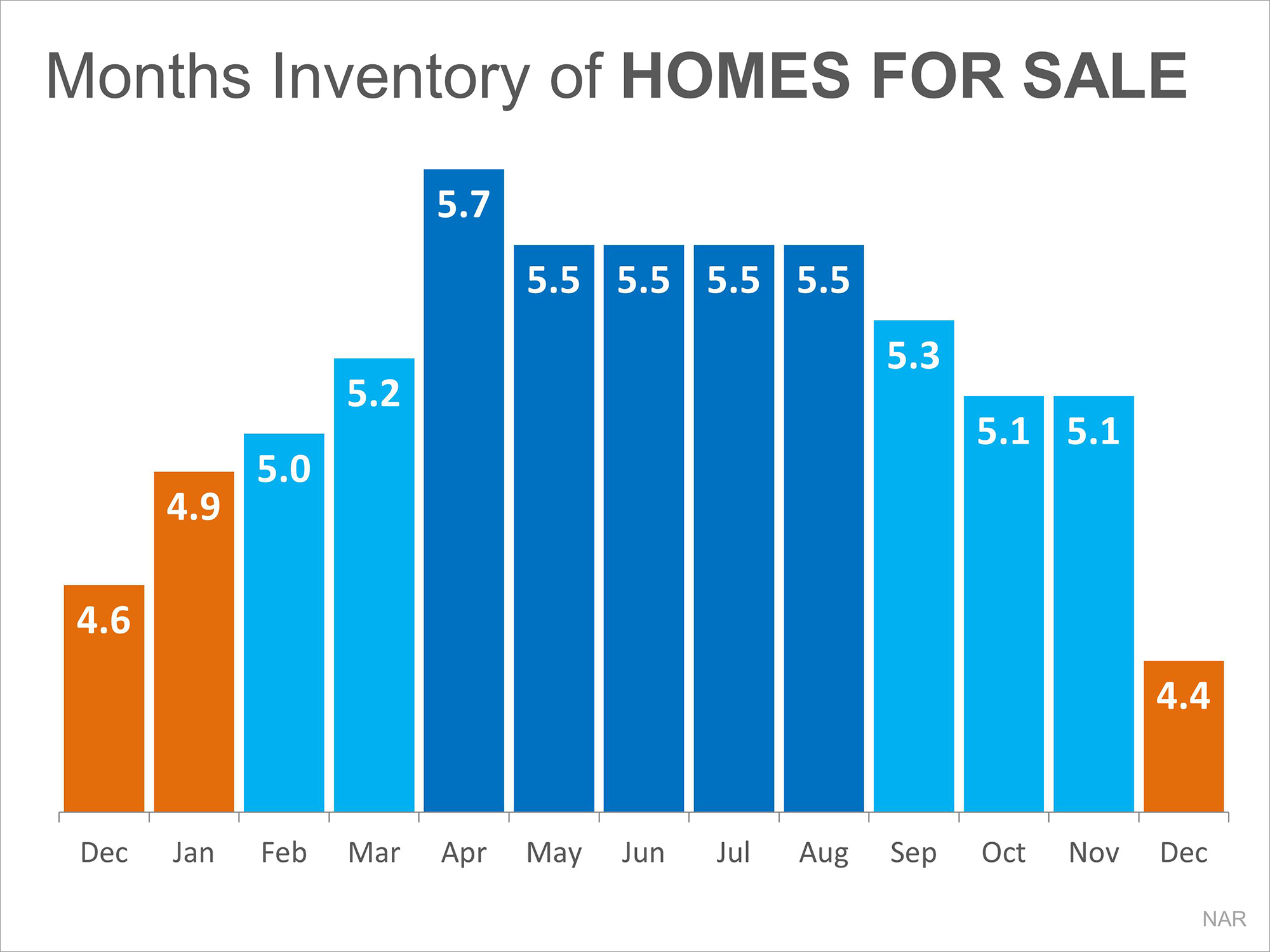

SUPPLY

The most recent Existing Home Sales Report from NAR revealed that the months’ supply of housing inventory had fallen to 4.4 months which is the lowest it has been in over a year.

Bottom Line

Listing your house for sale when demand is high and supply is low will guarantee the offers made will truly reflect the true value of your property. If you or someone you care about is interested in getting a better understanding of today’s market and where it stands, please don’t hesitate to contact me.

As I enter my 26th year in real estate, please know I stand ready and highly capable to help you and your referrals.

2015: A Year of Housing Opportunity

Many believed that when the housing market crashed, so too would the desire of American’s to own a home again. Many reports have shown that, especially among younger generations, the American Dream of homeownership is still very much alive.

Julián Castro, Secretary for HUD, recently summed up what it means to own a home in a speech at the National Press Club.

“Homeownership is still the cornerstone of the American Dream — a fact you can see in the lives of everyday folks.

It’s a source of pride. It’s a source of wealth, providing both a nest and a nest egg. And it strengthens communities and fuels growth in the overall economy.”

Castro appropriately named his speech, “2015: A Year of Housing Opportunity”, a theme that rang true throughout.

“Opportunity is not an abstract concept – it’s a path to a more prosperous life, and housing often serves as its foundation. T.S. Elliot once said that “home is where one starts from.”

“A home is often a primary source of wealth in a family… Having a home is generational way to pass that wealth on. We want people responsible enough to own a home to have that opportunity.”

Bottom Line

“Over the years-through decades of economic downturns and wars-the American people have always held on to this Dream, and always will.”

As the economy continues to improve, more and more Americans will qualify for homeownership, allowing more families to obtain the American Dream.

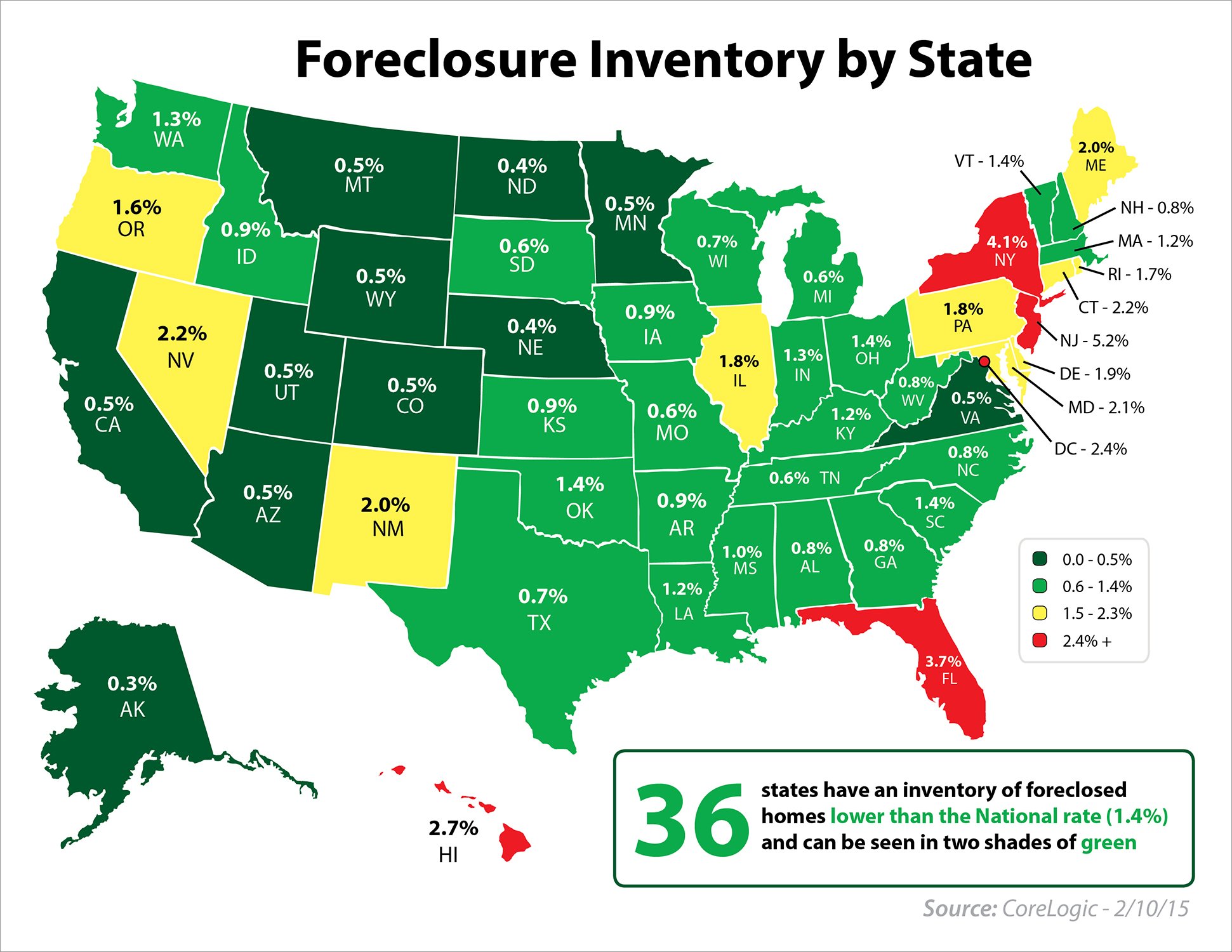

Foreclosure Inventory Down 34.3% from Last Year

According to the latest CoreLogic National Foreclosure Report, “approximately 552,000 homes in the US were in some state of foreclosure as of December 2014”. This figure is down 34.3% from the 840,000 homes in December of 2013. December marked the 38th consecutive month in which there were year-over-year declines.

Anand Nallathambl, the President and CEO of CoreLogic, is hopeful for the future, saying:

“At current foreclosure rates, we expect to see the foreclosure inventory in the U.S. drop below 500,000 homes sometime in the first quarter of 2015 which would be another milestone in the healing of the housing market.”

The map below shows the percentage of foreclosure inventory in each of the 50 states and Washington, D.C. Thirty-six states have inventory below the national rate of 1.4% and can be seen in two shades of green.

Bottom Line

Even though some states have not recovered completely from the foreclosure crisis, the nation as a whole is on the right track as inventory decreases.

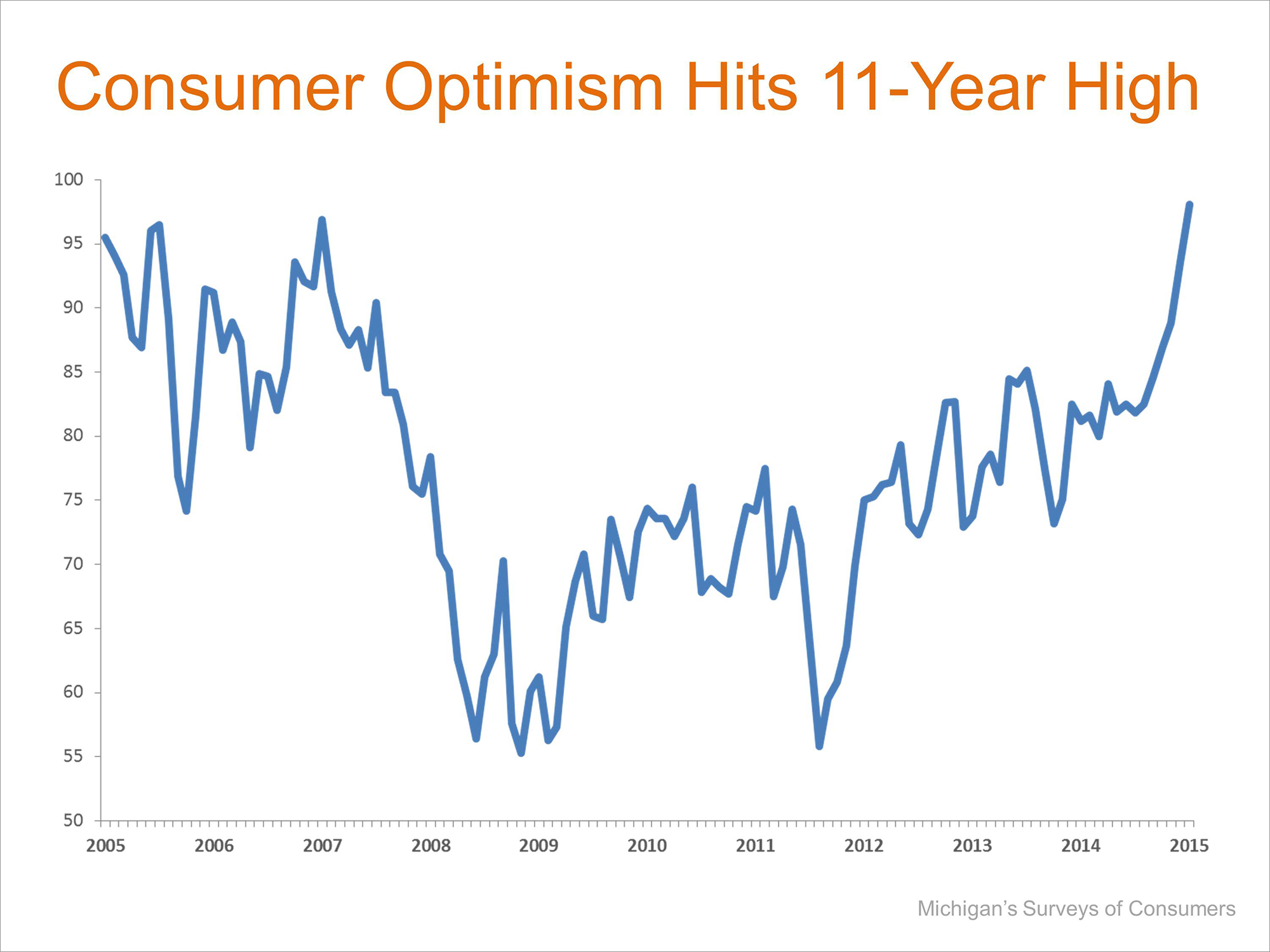

Consumer Confidence at Highest Level in Over a Decade

Two recently released reports reveal that the American public is starting to feel much better about the U.S. economy. The University of Michigan’s Surveys of Consumers showed that:

“Consumer optimism reached the highest level in the past decade in the January 2015 survey…Consumers judged prospects for the national economy as the best in a decade, with half of all consumers expecting the economic expansion will continue for another five years. The anticipated strength in the overall economy has been accompanied by more favorable income and employment expectations.”

Here is a chart showing results over the last decade:

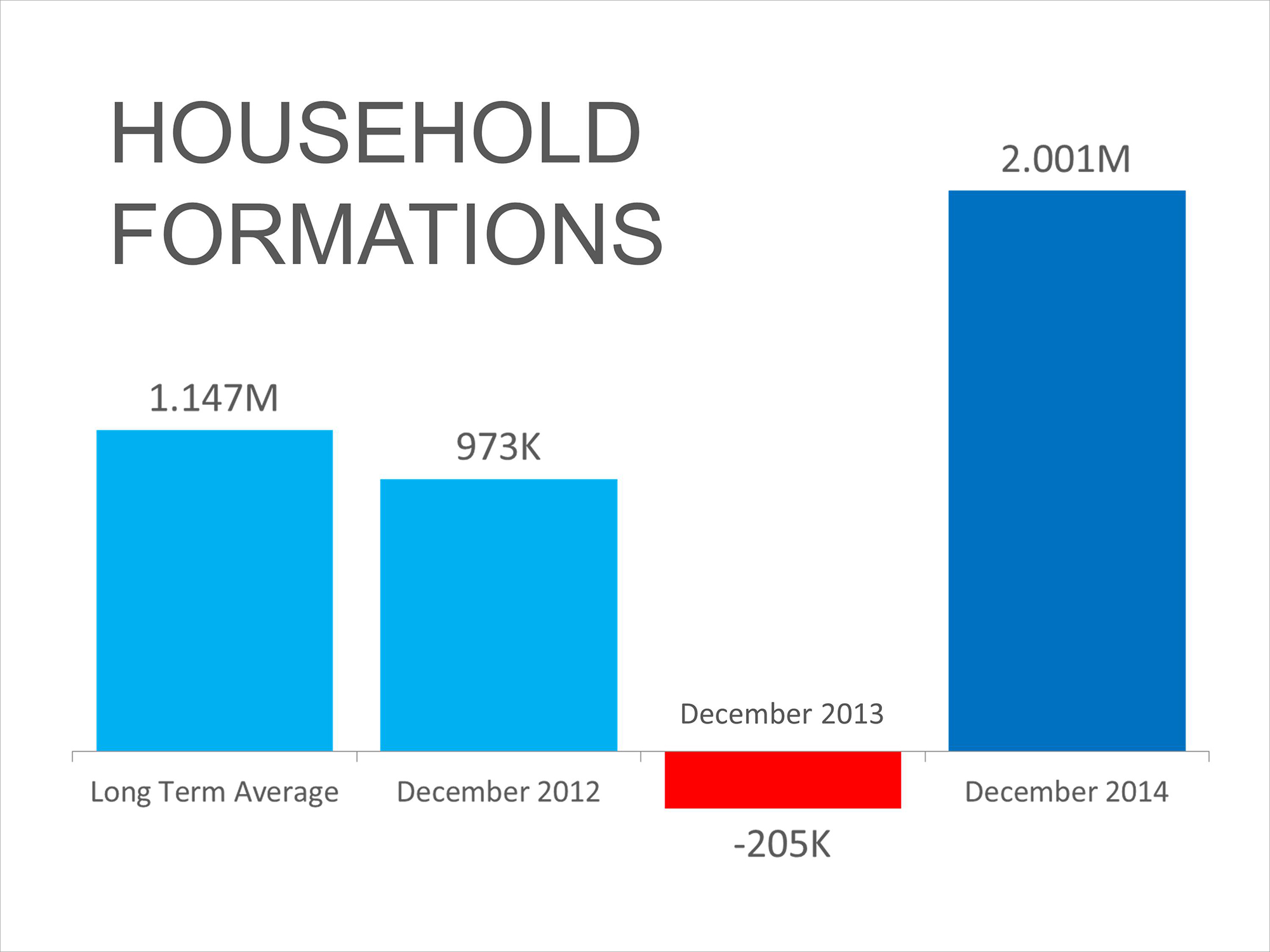

As all consumers are feeling more optimistic, more young adults are moving out of their parents’ basements and into a residence of their own. The recent Census report shows that new household formations skyrocketed in 2014. Below is a chart showing the historical significance of the numbers:

Bottom Line

The economy is definitely improving and, more importantly, the American consumer is beginning to feel much more confident. This should lead to a very robust real estate market in 2015.

Net Worth: A Homeowner’s is 36x Greater Than A Renter!

Over the last six years, homeownership has lost some of its allure as a financial investment. As homeowners suffered through the housing bust, more and more began to question whether owning a home was truly a good way to build wealth.

Every three years the Federal Reserve conducts a Survey of Consumer Finances in which they collect data across all economic and social groups.

Some of the findings revealed in their report:

- The average American family has a net worth of $81,200

- Of that net worth, 61.4% ($49,856) of it is in home equity

- A homeowner’s net worth is over 36 times greater than that of a renter

- The average homeowner has a net worth of $194,500 while the average net worth of a renter is $5,400

Bottom Line

There are many reasons why owning a home makes sense, the Fed study shows that owning is still a great way for families to build wealth in America.

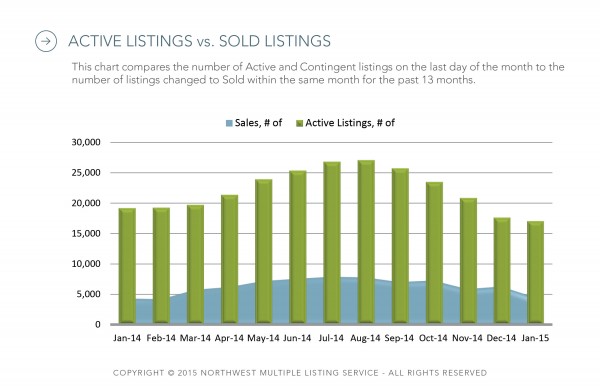

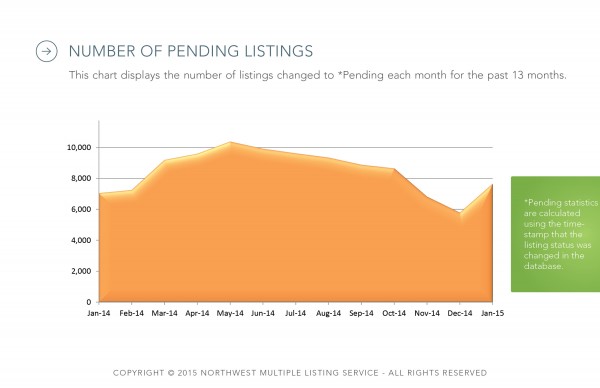

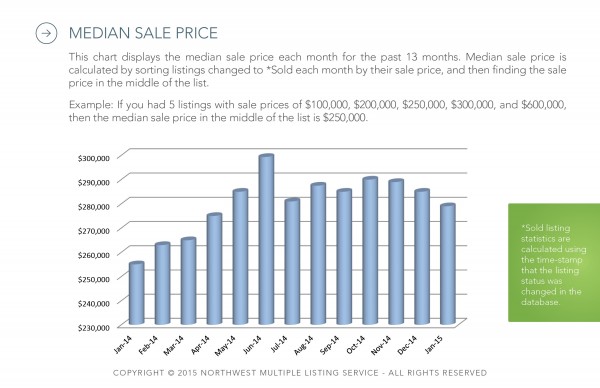

January 2015 Market Charts from the Northwest Multiple Listing Service

Here are the latest market charts from the MLS.

Click on each image below for a larger version.

Active Listings vs. Sold Listings

Number of Pending Listings

Median Sales Price

For more information our the Seattle and Eastside Real Estate Market contact Tony and Wendi Meier here:

[contact-form-7 id=”6″ title=”Contact form 1″]